When it comes to retirement spending, many people are familiar with rules of thumb, such as fixed annual withdrawal rates. While those guidelines can be helpful, they can feel abstract and don’t always accurately reflect how people actually think about their money.

The most common rule of thumb is the 4% rule. This rule suggests that you can withdraw 4% of your initial portfolio balance in the first year, adjust the percentage for inflation annually, and you will have a high probability of not running out of money during a 30-year retirement.

The rule can be a good starting point for people to conceptualize safe withdrawal rates, but it has its limitations.

- It is based on historical U.S. market data. It assumes future stock and bond returns, inflation, and interest rates will be similar to the past. This may not be the case.

- It assumes a static portfolio asset allocation. It is usually based on a fixed allocation of anywhere between 50-75% stocks and 25%-50% bonds. Your portfolio may look different than this and your asset allocation will likely change throughout your retirement.

- It assumes a fixed, linear spending pattern. In reality, retirement spending will fluctuate with life circumstances. For example, people tend to travel more in the early years of retirement which may drive higher spending. Toward the end of retirement, the last few years of life may be more expensive with healthcare costs. Spending rates are nonlinear in reality and require flexible planning.

- It doesn’t account for changes in your taxes or income. Some key considerations related to this: What age did you or will you start taking Social Security at? Are you eligible for survivor benefits if/when your spouse passes? When do you have to start taking Required Minimum Distributions (RMDs) from you IRA? Does that amount push you into a different marginal tax bracket?

In our experience, a more practical approach is to focus on combining numerical rules-based withdrawals with qualitative guidelines. That’s where the “Four L’s” of retirement spending come in: Lifestyle, Longevity, Liquidity, and Legacy.

Lifestyle is about your day-to-day living. Housing, travel, hobbies, and the experiences that make retirement enjoyable. This category is typically the most flexible and can be adjusted over time.

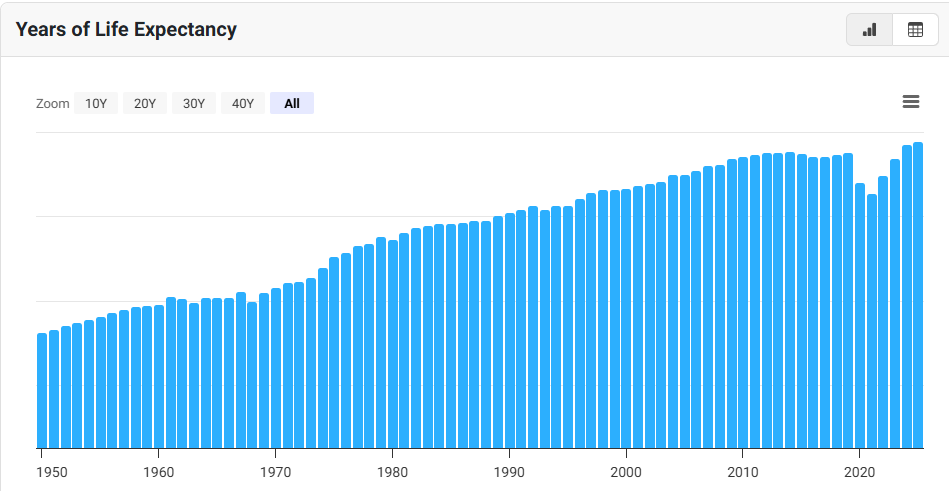

Longevity addresses the reality that retirement may last for decades. Lifespans have been increasing over time and people are spending a longer portion of their life in the drawdown phase. U.S. life expectancy at birth for men is 76.5 years and 81.4 years for women (Source).

Liquidity focuses on access to funds when you need them. Unexpected expenses (healthcare, home repairs, helping family) require having assets that are readily available without disrupting your long-term strategy.

Legacy reflects what you’d like to leave behind, whether that’s for family or charitable giving. Planning for this early can help ensure your intentions are carried out efficiently and thoughtfully.

It’s important that your financial professional works closely with your estate attorney to ensure your wishes are aligned and carried out as intended. Keeping beneficiary designations up to date is a key part of this process. We recommend reviewing your beneficiary designations on a regular basis, and more often after major life events, for accuracy and completeness.

Effective legacy planning means thinking about your assets across two distinct time horizons: supporting your needs during your lifetime and determining how those assets will be passed on after you’re gone.

Ultimately, your retirement spending plan should be tailored to your unique situation and use a combination of quantitative and qualitative factors to support your individual goals.

If you have questions about your own plan or would like to review how your current strategy aligns with your goals, please don’t hesitate to reach out.

Ashlyn Tucker, CFA, CDFA, M. Fin

ashlyn@rmhinvestment.com

Richard Mundinger, CFA

richard@rmhinvestment.com

520-314-2300

This newsletter is for educational purposes only, this is not investment advice.